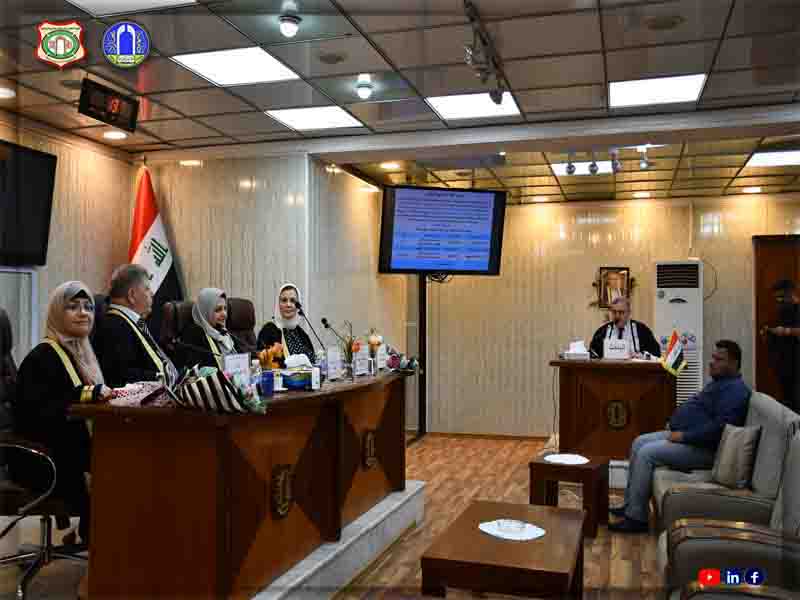

Institute media

The Department of Accounting Studies at the Post-graduate Institute for Accounting and Financial Studies at the University of Baghdad discussed the research titled(Accounting and reporting on retirement benefit plans according to the standard International Accountant (26) and its reflection on audit procedure-.Applied research in the State Employees’ Pension Fund) ) for the student Asl Ibrahim Mohammed to obtain chartered accountant certificate, which is the highest professional certificate in the field of specialization, and its holder enjoys all the rights and privileges of a doctorate degree.

The study aimed to apply International Accounting Standard No. (26) (Accounting and Reporting on Retirement Benefit Plans) in the State Employees Retirement Fund in accordance with the State Employees and Public Sector Salaries Law No. (22) of 2008 “amended” and the Unified Retirement Law No. (9) of 2014 “amended” in line with the unified accounting system.

The study concluded that the absence of an actuarial expert and actuarial applications in the State Employees Retirement Fund, which helps in developing hypotheses and actuarial assessments for demographic and financial variables, would make the pure application of International Accounting Standard No. (26) (Accounting and Reporting on Retirement Benefit Plans) in the Retirement Fund flawed and inaccurate in data.